Climate Insurance

2021-08-20

Insurance is an important aspect to consider if you wish your property to be sustainable. The rising number of extreme weather events due to climate change and the increasing cost of damages as a result of these events, make climate change a factor that profoundly affects insurance companies, and eventually their customers (us).

In this blog post, we attempt to help you become aware of risks your property is exposed to and the types of insurance available, alongside their coverage, their cost and potential options for cost reduction.

In this blog we cover:

The Risks Your Property Is Exposed To

Wind Insurance

Wildfire Insurance

Flood Insurance

Earthquake Insurance

Additional Opportunities For Discounts

Climate Insurance Is Changing

Insurance Companies Have the Power to Make a Change

References

The Risks Your Property Is Exposed To

Insurance is a form of risk management. The first step in the risk management process is identifying the risk. What are the risks that extreme weather events or other environmental hazards introduce to your property? Most of us are pretty much aware of the main climate risks in the location we live in. It is well known that California, for example, is at a high risk for earthquakes and fires. Still, some locations are less famous for their climate risks.

Heare at eampact you can find the prominent and relevant risks in the location of your property based on FEMA's NRI tool.

There are other tools out there: here you can find maps that specify which states in the U.S. are at high-risk for hurricanes, tornadoes, floods, fires, and earthquakes.

Another tool that can be helpful is an interactive map put together by the National Association of Insurance Commissioners (NAIC). By clicking on a specific state on the map, you can find relevant information for resilience in the face of high-risk disasters. in the chosen state.

Once you determine the risks in the location of your property, you can figure out the possible damages that can occur to buildings due to the following extreme weather events (find a more thorough overview of this topic in our blog post about the impacts of extreme weather events on buildings):

- Increased precipitation can lead to:

- Water damage to the foundation, envelope, or roof of the building.

- Flooding of low-lying areas (buildings with no elevation, below the normal altitude, or located close to water level).

- Long and severe droughts can lead to fires

- Severe storms such as Hurricanes and Tornadoes can lead to:

- Damage or degradation to building and infrastructure

- Overload and backup of storm-water drainage systems

- Flooding

- Earthquakes: the potential structural damage and destruction caused by a major earthquake is obvious, but even minor earthquakes can pose a risk as they lead to the weakening of structure over time.

Are You Covered?

Once you are aware of the risks and damages that may affect your property, check whether or not your insurance provides coverage for those risks.

If you have home insurance already, the information on what your coverage includes can be found on the declaration page in your insurance policy. This section also specifies what parts in the house are covered and for what type of damage.

Usually, home insurance covers damages from:

- Wind (hurricanes and tornadoes)

- Fires

But excludes coverage for damages from:

- Floods

- Earthquakes

Read on for in-depth details.

The Insurance Information Institute (III) put together a video that clearly explains homeowners insurance.

Considering Additional Climate Insurance

In many cases, if your home insurance does not sufficiently cover the risks relevant to your location, you can purchase additional insurance for specific climate risks. We gathered information on several types of climate insurances:

Wind Insurance

Generally, homeowners insurance includes coverage from windstorm damage in inland areas in the U.S. The homeowners insurance coverage includes damages from:

- Wind

- Hail

- Wind-driven rain

- Fallen trees due to high winds

However, in coastline states which have areas with a high-risk for wind, insurance companies require a percentage of the hurricane deductible instead of a flat dollar deductible. This means that the policyholder will pay a percentage of the home’s insured value before the coverage kicks in. Usually, the percentage varies between 1%-5% and sometimes even higher, depending on the level of risk in the property’s location.

According to the Insurance Information Institute (III), 19 states in the U.S have percentage deductibles and they provide information on the deductibles by state.

Some areas are at too-high risk for wind and storms, which means that insurance companies can refuse to offer insurance. In such cases, many states offer FAIR Plans, which are state-mandated programs for those who are struggling to find insurance. Beach plans are FAIR plans that are specific to windstorm coverage, but these plans may be more expensive.

Annual windstorm premium ranges widely between $600 to $2,000. The average differs by state and varies based on the location of the property, whether it is in a high-risk area, the age and condition of the property, and the crime rate in the area. Florida has the highest average annual premium of $2,000, and in some locations such as Miami, the premium can be higher than $4,000.

Luckily, Florida requires insurance companies to offer discounts on windstorm insurance for properties with wind-resistant features by qualifying for wind mitigation credits. Wind mitigation credits can reduce up to 40% of the premium, if specific features are added, such as:

- Impact-rated glass on doors and windows

- Hurricane shutters

- Reinforced roof-to-wall connections

- Roof-deck attachments.

Wildfire Insurance

As mentioned, most standard homeowner insurances cover damages from fires. The coverage includes the:

- Building structure

- Any attached and detached structures

- The landscape

- Personal belongings

- The content of the building

- Cost of temporary accommodation in case your house is unlivable

In the policy, you can find the standard limits of the coverage, and you can choose to increase the coverage limit if you feel it is not high enough.

Note that homeowners insurance typically doesn’t cover damages from fires that were started deliberately by the owner or fires that were a result of an act of war or a result of nuclear radiation. Another exclusion is a vacant house that has been vacant for more than 30 days. In such cases, there are specific policies for vacant houses.

As with windstorms, areas that are highly exposed to wildfires can sometimes struggle to get insurance. The unprecedented fires in California in recent years has resulted in the refusal of insurance companies to renew home insurance. If you are struggling to get fire insurance, California offers Fair Access to Insurance Requirements (FAIR) plans.

If your property is located in a high-risk area for wildfires, having insurance is a good idea. Another good idea would be to take necessary measures to protect your home from wildfires, such as:

- Keeping combustibles away from your house and clean your roof and gutters regularly

- Choosing materials wisely, such as pebbles instead of mulch for landscaping

- Planting high-moisture annuals and perennials native to your area

- Using non-combustible siding, fences, and gates

- Getting a Class A fire-rated roof

- Using multi-pane, tempered glass windows

Flood insurance

According to FEMA, floods are the most common natural disaster in the U.S., which may be the reason why most insurance companies exclude flood damages from their homeowners’ insurance coverage. However, flood insurance can be purchased separately.

In some cases, you will be required to purchase flood insurance. If your property is located in a high-risk flood area and your mortgage lender is federally regulated or insured, the lender is mandated to require flood insurance. The lender can also decide to require flood insurance even if they are not mandated to.

The National Flood Insurance Program (NFIP) provides flood insurance to property owners, renters, and businesses to assist with a fast recovery when floodwaters recede. The NFIP insurance is mandatory in Special Flood Hazard Area (SFHA), which may lead to the misperception that areas outside of the SFHA are not at risk of flooding. It is important to note that some experts consider FEMA’s flood maps to be outdated, therefore not an accurate representation of the true flood risk in certain areas.

The NFIP’s insurance can be purchased from private insurance companies, but the federal government is still responsible for underwriting losses.

NFIP insurance provides two separate policies:

- Building Property Coverage: a policy for the building itself

- Personal Property Coverage: a policy for the content of the building

You can choose to purchase both policies or a single policy.

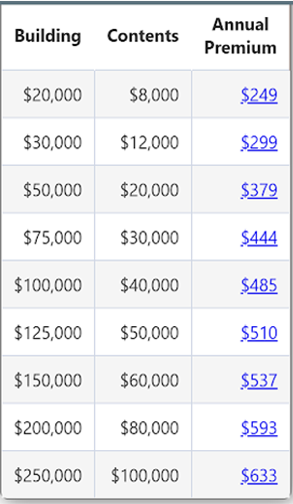

We looked at flood insurance from Allstate as an example:

Building property coverage provides coverage for the physical structure of your home or non-residential property, including electrical and plumbing systems, refrigerators, window blinds, and more. The maximum coverage in this policy is $250,000.

Personal property (contents) coverage provides coverage for the items inside your home, like clothing, furniture, and electrical appliances at their value during the time of loss. This policy’s coverage is limited to $100,000.

Both policies do not cover:

- Damage caused by moisture, mildew, or mold that could have been avoided by the property owner

- Currency, precious metals, and valuable papers like stock certificates

- Property and belongings outside of a building like trees, fences, and swimming pools

- Living expenses like temporary housing

Factors such as the location of the property (whether it is in a high-risk zone or not) and the age of the property can impact the cost of flood insurance. Currently, the average cost is $700. You can also search for calculated premium averages by state.

Here is an example of an instant quote from GEICO for a residential home that is not located on the water. The premiums are set by the NFIP and therefore will be similar in other insurance companies. For homes with values higher than $250,000, you will need to contact the insurance company to get a quote.

As of October 1st, 2021, FEMA will update the NFIP pricing methodology for the first time in fifty years. The new methodology will incorporate more flood risk variables such as flood frequency and type, the distance of the property to a water source, and specific property characteristics such as elevation and cost to rebuild. New policies beginning October 1st will be subject to the new rating methodology and existing policyholders eligible for renewal will be able to take advantage of immediate decreases in their premiums.

Note that flood insurance has a 30 day waiting period after its purchase before the coverage takes effect, so don’t wait until the last minute to purchase.

One way to reduce the cost of your flood insurance is to enroll your community in the Community Rating System (CRS) which is an incentive program provided by the NFIP. The city of Livermore, for example, received a 20% discount on flood insurance by making their city more flood resilient.

Another way is to retrofit your house to make it more resilient to floods by:

- Elevating your property, or at least elevating the utilities and HVAC equipment to higher levels if possible

- Installing a sewage water backstop

- Including porous surfaces in your landscape

Earthquake Insurance

Homeowner insurance (for property owners with a mortgage) doesn’t cover damage from earthquakes unless it is a fire caused by an earthquake. Yet, homeowners insurance is obligated to offer additional earthquake insurance for purchase.

The cost of earthquake insurance varies according to location, age, and size of the property, and can range between $300-$4,000 per year.

The cost of the insurance increases as your risk increases. Both will be higher if your property is older, built of brick or masonry, or has more than one story.

Earthquake insurance will usually cover:

- Dwelling coverage - the cost of rebuilding or repairing your home after it is damaged by an earthquake.

- A place for you to live while your home is being repaired due to an earthquake, or needs to be evacuated. The large insurance companies limit this payment to a minimum of $100,000.

- Personal property such as furniture and appliances. Payments range between $5,000 and $200,000.

Earthquake insurance will usually not cover:

- Anything that your homeowners insurance already covers

- Landscapes or damages to your land

- Pools

- Masonry

- Separate buildings

- Flood damage caused by earthquakes

Once again, by adding features to your home that can protect it and your family from extreme and minor earthquakes, you can reduce your home insurance by up to 20%.

Examples of features that can reduce the cost of earthquake insurance are:

- Bolting your house to the foundation

- Bracing the chimney

- Bracing the water heater to a wall

- Installing automatic gas shut-off valves

- Strengthening cripple walls with plywood

Additional opportunities for discounts

Insurance for climate change can be a financial burden, especially at a time when extreme weather is increasing and insurance premiums increasing along with it. Homeowners insurance has increased by 59% in the past decade and is predicted to continue increasing in the coming years.

Here are some additional opportunities that can lower your climate insurance premium:

- You can save an average of 35% on your home insurance if you purchase a newly built home, 19% by bundling your home and car insurance, and up to 11% by choosing superior or fire-resistant materials.

- Some insurance companies offer a 5-10% discount on home insurance for LEED-certified homes. Note that green-certified buildings may also have other insurance costs embedded.

- A few states offer discounts and credits for homes that are certified resilient through FORTIFIED standards.

- Some climate change insurance companies provide endorsements for eco-friendly replacement materials. After a loss, these allow the insured to replace or rebuild with more sustainable materials, practices, and products.

- For homeowners who generate their own geothermal, solar, or wind power, and sell any surplus energy back to the local power grid, know that some policies cover both the extra expense of temporarily buying electricity from another source and the income lost during a power outage.

Climate Insurance is Changing

In recent years there is an ongoing trend in the insurance world to include sustainability and climate change in their risk assessment and policies.

In July 2018, the International Association of Insurance Supervisors (IAIC) released a paper on Climate Change Risks to the Insurance Sector, in which it concludes that it is imperative that all insurers consider their exposure to climate risks, regardless of size, specialty, domicile, or geographic reach, and that they seek to build resilience to such risks where appropriate.

- Sustainable Insurance Forum (SIF) established in 2016 is an international network of insurance regulators and supervisors, working on sustainability challenges. Early in 2020, the NAIC joined the forum.

- A few dozens of insurance companies from around the world signed the United Nations PSI (Principles for Sustainable Insurance) in which they declare that those insurance companies make an effort towards sustainable ESG (Environmental, Social and Governance) goals. Note that this commitment is not bound by law and those companies can be easily removed from the list if they don’t fulfill their obligations.

- ClimateWise attempts to help its 40 members, which include big insurance companies, to directly support society as it responds to the risks and opportunities of climate change.

- Insuresilience Solutions Fund (ISF) fosters the development of needs-based and financially sustainable climate risk insurance products in developing and emerging countries, increasing the resilience of poor and vulnerable households against extreme weather events and natural catastrophes for homes in developing countries.

- The Munich Climate Insurance Initiative (MCII) Is focused on developing solutions for the risk posed by climate change for the poorest and most vulnerable people in developing countries.

Insurance Companies Have the Power to Make a Change

For homeowners and business owners, insurers can significantly influence risk-reducing behaviors.

Insurance companies can decide to direct capital to reduce emissions, adaptation, and resilience in the face of climate change. They have strong influencing power, and by making collaborative decisions with other insurance companies, they can make a positive change. They can influence the behavior of individuals, businesses, and governments.

Will Climate Insurance Last?

Yet, insurance companies can’t fix or finance damages from all disasters. In fact, insurance covers just one-fifth of all disaster-related losses. The federal government had to increase the disaster annual budget many times in the last 30 years. The burden on insurance companies is becoming unbearable.

As mentioned, Californians who struggle to get fire insurance can default on FAIR programs. FAIR programs are offered in about 30 other states, and their demand is increasing since insurance companies are retreating from high-risk locations.

Moreover, lenders are selling risky loans to other mortgage corporations. This transfer of risk from hand to hand is similar to the Subprime crisis and may end at a similar result.

So if the home insurance industry is in trouble due to climate change, who can we turn to? The answer is maybe no one, maybe it’s time to take matters into our own hands. We should make sure we are aware of the risks we are exposed to and are prepared for them. Now, our focus should be on improving our home’s resilience to natural disasters so we can be prepared when disaster strikes.

Conclusions

- In general, even if an insurance company covers damage from an extreme weather risk, if your home is in a high-risk location, the insurance company may either not include that specific risk in their coverage, or they will offer it at a high premium and/or with very little coverage. This makes sense since, in high-risk zones, the cost of repairing the damage is too high for the insurance companies to handle. Therefore, their strategy is to narrow the coverage, or up the premium. In reality, they do both.

- Many states realize that high-risk areas may struggle with purchasing insurance and offer Fair Access to Insurance Requirements (FAIR), or Beach Plans.

- Insurance premiums may vary according to many aspects including location, construction (design and materials), condition of your home (age, wear and tear), and the number of historical claims.

- It is important to note that claims due to extreme weather catastrophes usually take a long time to process. The reason being is that usually after a catastrophe, many properties are damaged in a certain area at the same time. This puts a significant burden on insurance companies who need to service many claims simultaneously. A helpful piece of advice is to notify your insurance company immediately, and while you wait impatiently for the claim to be processed, take photos of all the damage and document everything.

- Lastly, we’ve seen that if you increase your home’s resilience by adding specific resilient features, you can decrease the cost of insurance. These resilient features better protect your property and reduce the risk of additional costs from potential damage. If there is no insurance coverage in your area for certain risks, leveraging climate adaptation strategies against those said risks may be the only solution.

KEEP COOL. BUILD RESILIENCE. EAMPACT.

References

- How To Protect Your Home From Extreme Weather - Reviews.com

- CIPR State Resiliency Map (naic.org)

- Earthquake Damage: What It Can Do to Your Home? (hudsondouglaspublicadjusters.com)

- Homeowners’ insurance explained https://www.youtube.com/watch?v=PUZSIahxq-g&feature=emb_logo

- Background on: Hurricane and windstorm deductibles | III

- The FAIR Plan Explained and How to Get This Policy

- Florida Wind Insurance & How to Lower Costs with Wind Mitigation Credits

- Insurance for wildfires | III

- After 2017 fires, more Sonoma, Mendocino, Lake homeowners turn to California for Insurers refused to renew homeowner policies insurance coverage

- California FAIR Plan Association

- Facts about wildfires | III

- Work With the National Flood Insurance Program

- Special Flood Hazard Area (SFHA)

- US Private Flood Insurance: The Journey to Build a New Market

- FEMA’s Outdated and Backward-Looking Flood Maps

- Write Your Own Flood Insurance Company List

- Flood Insurance/ Allstate

- How Much Does Flood Insurance Cost in 2020?

- National Flood Insurance Program Community Rating System

- Livermore Receives Major Flood Insurance Discount for Residents

- FloodSmart | Ways to Pay Less for Flood Insurance | FloodSmart - Agents

- 11 Safety Features That Can Lower Your Homeowners Insurance Premiums

- Climate change and home insurance

- Home insurance discounts can save you hundreds

- Insurance for Green Buildings

- FORTIFIED and mitigation credits, insurance discounts, tax credits, tax deductions, and funding.

- Front - FORTIFIED Home™

- Climate change risk to the insurer sector/IAIS https://docs.wixstatic.com/ugd/eb1f0b_0e5afc146e44459b907f0431b9e3bf21.pdf

- SIF | Sustainable Insurance Forum (SIF)

- Sustainable Insurance Forum https://b9ea8c1e-dc19-4d5f-b149-9b1ea4b8d050.filesusr.com/ugd/eb1f0b_ebfd5d2dd1914be584f6e9ddd77093fc.pdf

- Signatory companies « UNEP FI Principles for Sustainable Insurance

- ClimateWise — Cambridge Institute for Sustainability Leadership

- About ISF – Insuresilience Solutions Fund

- The Munich Climate Insurance Initiative https://climate-insurance.org/about/

- Global insurers unite/ Oceana https://www.unepfi.org/psi/wp-content/uploads/2017/10/PSI-Oceana-press-release.pdf

- Disaster Mitigation: How Incentives Can Help

- Insurance companies and lenders are responding to climate change — by shifting risk to taxpayers

- 16 factors that affect home insurance rates

- 10 facts you should know about weather-related home insurance claim

Add a Comment

Please leave a reply.Your email address will not be published.

Comments

Relevant & Trending

Climate Resilient Boulder

2022-04-28Sacramento Confronts Flood and Drought Risks

2021-09-07How does the environment impact our homes

2021-09-12Community Resilience

2021-09-12Keeping Our Heads Above Water

2022-08-04Climate Resilient Austin

2022-04-29Here Comes the Rain Again

2023-10-03Earth Is a Gift We Must Reciprocate

2022-01-25