When Hail Freezes Over

2022-09-30

Hail is a form of solid precipitation consisting of ball-shaped chunks of ice, individually called a hailstone. Hailstones are formed when raindrops are carried upward by thunderstorm updrafts into extremely cold areas of the atmosphere and freeze.

Smaller hailstones can be blown away from the updraft by horizontal winds, while larger hail typically falls closer to the updraft.

The potential damage from Hail

Hailstones generally become destructive when they are about the size of a quarter or larger. Once they reach that size, they can cause extensive damage to homes, vehicles, and other residential structures. Hail causes billions of dollars of property damage to cars, homes, and crops annually. The annual damage from hail in 2019 and 2020 averaged $8 billion and $14 billion respectively.

Wind-driven hail can tear up roofs and siding of houses, break doors and windows, blow into homes and cause severe injury or death to people and animals.

In North America, hail is most common in the area where Colorado, Nebraska, and Wyoming meet, known as "Hail Alley". Hail in this region occurs between March and October during the afternoon and evening hours. Cheyenne, WY, is North America's most hail-prone city, with an average of nine to ten hail storms per season.

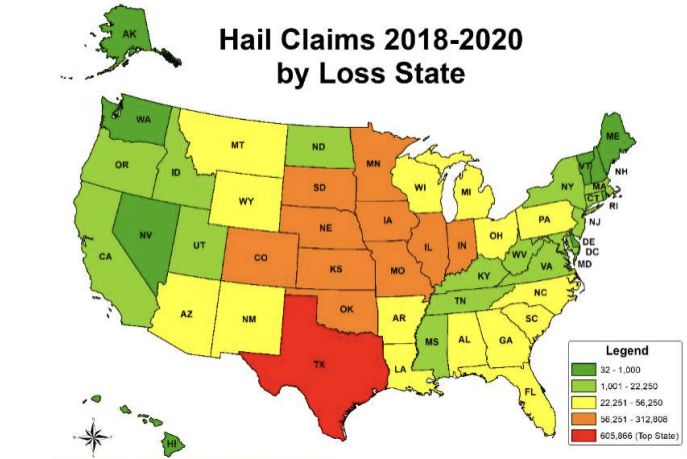

However, A report by Verisk shows that while the “hail alley” region is at significant risk, hail exposure is expanding and now demands attention in all states. The National Insurance Claim Bureau (NICB) provides data on claims in the U.S from 2018 to 2020. The following map shows that Texas had the highest increase in hail claims from 2018 to 2020. The Verisk report ranked Texas first in 2020, with more than 1.5 million properties affected by one or more events, for a total of $3.3 billion in claims.

Overall national hail claims from 2018 through 2020 increased two percent from 832,377 to 849,033.

The report further states that 6.2 million properties in the U.S experienced at least one damaging hail event in 2020, and the claims that year resulted in almost $14.2 billion in losses.

Besides reiterating the need to address the risk in all states and the unpredictability of hail occurrences, the report emphasizes that sometimes hail claims are filed long after occurring because the damage to the roof, which is the most vulnerable element in the house to hail, can stay hidden from the eye.

The Rocky Mountain Insurance Information Association (RMIIA) provides information on hail in general and on hail claims in particular.

Insurance

While typically, hail damage is covered by homeowner’s insurance in most States, in some coastal regions, hail coverage is not guaranteed. In hurricane or windstorm-prone areas, you may need a separate windstorm deductible, which can range between one and ten percent of the dwelling coverage. In some cases, instead of a separate deductible, the coverage is limited and the premiums are increased.

In this article, you can find information on filing a hail claim.

Insurance is always a good idea, but it’s not a solution for preventing damage.

Favorable consideration would be to apply resilience strategies to your home.

Hail Resilient Strategies

Roof

The roof slope is an vital factor when considering the damage from hail. A steeper slope may reduce overall hail damage if the hail falls vertically to the roof. Damage to the part of the roof not facing the wind can be very limited or avoided. Note that in hurricane and tornado-prone areas, steep roof slopes are less recommended due to the “sail effect.” Therefore, you should study your risks well and consult a professional on the resilient strategies and tradeoffs between these two risks.

Whether a new home or an existing one in need of a roof replacement, consider using hail-proof roofing materials. The American Society for Testing and Materials (ASTM) and the Underwriters Laboratories (UL) have developed standard protocols and testing to ensure products, such as roof shingles, can withstand hail.

If your roof has shingles, they will drain rainwater and prevent piling snow, but not all shingles can resist hail. Impact-resistant shingles, such as Owen’s Corning’s products, are hail-resistant shingles that should be installed in areas prone to hail and strong winds. Impact-resistant shingles can resist greater impact without cracking or breaking, and may even reduce insurance costs. Such shingles may convey insurance companies to provide discounted premiums.

When replacing a roof or installing a new one, consider installing full roof underlayment, such as these roof deck protection by GAF. The underlayment can help protect from water penetration.

Sidings

Although the roof is the most vulnerable house element to hail, the sidings can be vulnerable as well. If the winds are strong enough, hail can fall at an angle or nearly horizontally. Wind-driven hail can tear up sidings.

Make sure that you choose hail-resistant materials for the sidings, such as fiber cement board, used in James Hardie’s siding, or engineered wood, used in LP Corp’s Sidings.

Windows

Hail can damage windows by breaking the glass, putting in danger the occupants in the house. Hail can also damage the sashes, grills, and even window frames. Therefore, extra precautions to protect your windows would be an essential and wise investment.

As with roofs and sidings, for skylights, windows, and doors, choose materials that withstand high debris impact. Marvin’s coastal windows, for example, meet the stringent Miami-Dade County requirements.

Another strategy that helps avoid the hazards of shattered glass is installing storm shutters. Closed storm shutters can protect and secure your windows from a hailstorm. Since hail can strike unexpectedly, install storm shutters that can remain in place all year.

Window film is another layer of protection for your windows. Such films make the windows harder to break, protecting them not only from hail, but also from water penetration, UV, and even theft, and will improve your energy efficiency.

Final Thoughts

Hail can occur at unexpected times and locations and can cause damage to your property which can lead to financial losses and even injuries to occupants.

Although hail damage is usually covered by homeowner’s insurance, in areas with a higher risk of hail, you should expect higher premiums or separate deductibles, and in some cases, the damage can be hidden for a long time before being detected, which might be too late to file a claim.

Therefore, even if you live in an area not at high risk of hail, it’s a good idea to prepare your home to be protected from hail.

You can implement the mentioned solutions and strategies in your home to mitigate the risk of hail damage, mainly in the design and materials of your roof, but also in other house elements such as the sidings, windows, and doors.

Add a Comment

Please leave a reply.Your email address will not be published.

Comments

Relevant & Trending

How does the environment impact our homes

2021-09-12Climate Insurance

2021-08-20